Each year since its founding in 1944, CancerCare’s oncology social workers and financial navigators have spoken with thousands of people facing a cancer diagnosis. In the past few years, we have increasingly heard of the challenges our clients face in accessing their prescribed treatments because of their insurance plan restrictions.

Each year since its founding in 1944, CancerCare’s oncology social workers and financial navigators have spoken with thousands of people facing a cancer diagnosis. In the past few years, we have increasingly heard of the challenges our clients face in accessing their prescribed treatments because of their insurance plan restrictions.

We have created this guide, The Employer Toolkit, to address the impact of the roadblocks that are preventing patients from accessing the medications they so desperately need. Approximately 50% of Americans receive healthcare through their jobs, and those benefits are among the most important that an employer can offer its valued employees.

Many cost-saving measures seem benign but can cause great harm, particularly to those with cancer and other serious or chronic health conditions. In your efforts to control healthcare costs, it is important to ensure that the strategies you consider do not adversely impact your employees’ wellbeing. Looking at healthcare benefits holistically, however, helps to demonstrate how some cost-saving measures can actually increase overall healthcare costs and absenteeism, while also reducing productivity and causing other adverse consequences.

This Toolkit is designed to help explain the unintended consequences of increasingly common prescription drug cost control measures and offer recommendations on how to structure prescription drug benefits to protect your employees who need access to these medications. Several of our recommendations have become law in many states, which we believe supports the case for these measures. We approached this project from our perspective as a cancer organization, but the issues we highlight in this Toolkit apply to anyone facing a serious illness or dealing with a chronic condition.

We hope you will listen to the patients’ experiences featured in the Toolkit videos and help others – namely, your employees and their beneficiaries – avoid these or similar life-defining experiences, when facing a serious health problem.

Thank you.

Sincerely,

Patricia J. Goldsmith

CancerCare

Introduction

An Overview of Utilization Management (UM)

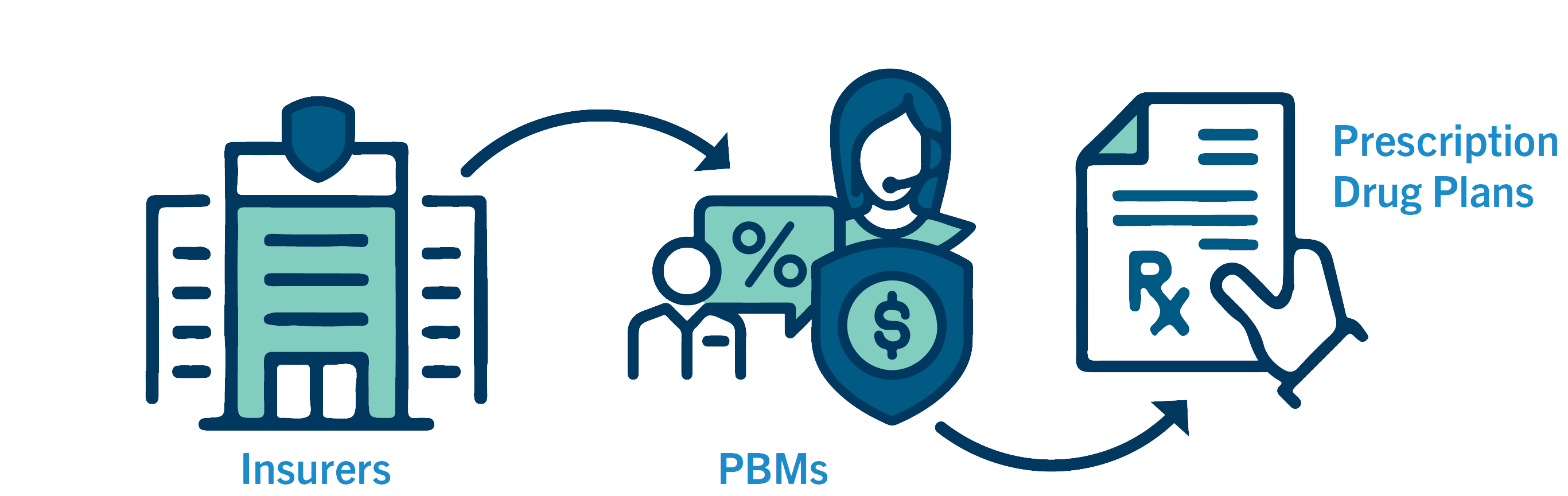

The Role of Pharmacy Benefit Managers (PBMs)

Innovations in Cancer Care vs. Utilization Management

The last decade brought significant breakthroughs in cancer care. New targeted therapies help match the unique genetics of a patient’s cancer cells with the right drug—one that will zero in on the cancer and leave healthy cells untouched. New immunotherapies train the immune system to better recognize and battle cancer cells, including

The last decade brought significant breakthroughs in cancer care. New targeted therapies help match the unique genetics of a patient’s cancer cells with the right drug—one that will zero in on the cancer and leave healthy cells untouched. New immunotherapies train the immune system to better recognize and battle cancer cells, including Working With Benefits Consultants

What Employers May Not Know

Despite having health insurance, many cancer patients suffer from

Despite having health insurance, many cancer patients suffer from The Cost of UM to Employers

Common Utilization Management Practices & Consequences

Common UM Practices & Consequences

Pre-authorization

What is pre-authorization?

In healthcare, pre-authorization (PA)—also called “prior authorization,” “prior approval,” and “pre-certification”—requires that certain services, treatments or prescriptions be submitted to the insurer for review and deemed medically necessary before the patient receives that care.23 Although intended to contain costs and protect patient safety,24 PA requirements can delay treatment, restrict access to medications or specialists and increase out-of-pocket costs for patients, who may ultimately abandon treatment.25

Joanna Morales, a cancer rights attorney and CEO of Triage Cancer, describes how securing PA adds stress for cancer patients and their caregivers during an already difficult time. “While healthcare providers may assist with pre-authorizations, at the end of the day the burden is on the patient. If a patient doesn’t get pre-authorization for a drug or treatment they’ve received, the insurance company can refuse to cover it. Then the patient may have to pay the full cost of that care.” Morales points out that since there isn’t a set list of drugs or procedures that require PA, patients have to be vigilant and proactive in seeking it. “And the rub is that even when you get pre-authorization, payment isn’t guaranteed.” Morales has known of insurers telling patients that pre-authorization “was just temporary and we can change our mind.”

An estimated 72-90% of all PA requests are approved, with additional approvals granted when patients appeal an initial denial.26,27 That sounds like good news at first. But given the delays and costs associated with PA, that high approval rate raises questions about what this process actually accomplishes. Unfortunately, the hassle of PA may be the point: some health plans use it as a deterrent or gatekeeper, knowing that even to get the care they need, many patients won’t pursue pre-authorization or appeal when it’s denied.

“And the rub is that even when you get pre-authorization, payment isn't guaranteed.”

- Joanna Morales

Cancer rights attorney & CEO of Triage CancerMany physicians report that PA policies are an obstacle to good patient care. According to the 2020 AMA Prior Authorization Physician Survey:

- 90% said pre-authorization has a somewhat or significant negative impact on patient outcomes.

- 94% reported that the process delays access to necessary care.

- 79% reported that it led to patients abandoning their recommended course of treatment.

- 30% reported that pre-authorization has led to a serious adverse event for patients in their care.

Pre-authorization & prescription drugs

Pre-authorization and prescription drugs

Increasingly, insurers have targeted prescription drugs for pre-authorization as a cost-saving measure. What started as requirements for new, high-cost specialty medications has grown to include even established brand-name drugs and generics with no low-cost alternatives.28 For example, more than quarter of drugs covered by Medicare Part D plans required PA in 202129; in 2007, it was just 8%.Physicians typically can’t tell if a medication requires PA when they prescribe it: that info isn’t readily accessible, varies by health plan and changes often. Instead, physicians submit requests retrospectively, after the pharmacy flags a coverage issue.28,30 But that added step deters many patients: 37% of prescriptions flagged for PA are abandoned by patients at the pharmacy and never filled.31

Treatment abandonment is one reason why PA is linked to worse health outcomes, increased hospitalizations and higher overall medical costs when it’s applied to drugs that treat diabetes, depression and other mental health conditions. These same serious and chronic illnesses—as well as cancer and multiple sclerosis—are now subject to PA requirements that cover entire disease states and classes of drugs under some health plans.28

Costs of pre-authorizations

Costs of pre-authorizations

Medical practices expend significant resources to secure pre-authorizations. In the 2020 AMA survey, respondents reported an average of 40 pre-authorizations per physician, per week. The extra administrative work takes away from physicians’ time spent caring for patients and contributes to physician burnout, which reduces the quality of care.32 Some physicians avoid prescribing certain treatments, even when they’re beneficial, knowing that the PA process will be particularly cumbersome.25As practices struggle to cover higher administrative overhead due to the PA process, the costs come back to patients. “You might see on a bill where a physician charged $300 for a 20-minute visit, and you think, ‘How can that be?!,’ but very little of that is profit,” explains oncologist Len Lichtenfeld, MD. “The majority goes to the costs of running a medical practice, including the extra administrative staff and other office overhead needed to handle pre-authorizations. What we see now are large networks buying up smaller practices. These networks have a stranglehold on services in large cities and can go toe-to-toe with insurance companies to negotiate better reimbursement. But that comes at a cost to patients, directly and indirectly. It comes in higher insurance premiums, higher prices for service, higher copays.”

What does pre-authorization accomplish?

What does pre-authorization accomplish?

Many physicians and patients experience an endless PA roller coaster. In a 2016 AMA survey, 80% of physicians reported they were frequently required to re-submit requests for on-going treatments that stabilize patients with chronic conditions, despite the finding that 72% of initial pre-authorization requests were approved.26 A study of dermatology clinics found the vast majority of biologic drug prescriptions were approved, yet the PA process cost clinics a median $15.80 per request and took as long as 31 business days.33 It begs the question: Should patients really wait a month for medications that are overwhelmingly authorized?Pre-authorization doesn’t save patients or employers money, and health economists question whether it actually saves health plans money either.

In some cases, administrative costs to the insurer outweigh any cost savings and plans actually lose money.34

Other studies have linked PA to increases in overall healthcare costs.35 In one, patients with Type 2 diabetes who were denied PA for newer medications had higher overall medical costs the following year, likely resulting from conditions that worsened without necessary drugs.36

Calls for reform ask why the time-consuming, repetitive PA process can’t be streamlined to benefit all involved since reducing the administrative load could save time and money for patients, physicians and health plans alike.37 A standardized electronic approval process and real-time decisions on commonly approved items could help. Employers can address this by selecting or customizing health plans that relax PA requirements, particularly for chronic conditions and time-sensitive illnesses such as cancer.

In response to this, under a recently passed Texas law, physicians will no longer be required to get prior authorization for common procedures or prescriptions where they have a 90% or better approval history.

Case study: Amy W.

Amy W.

Amy W.

Washington D.C. area

Multiple myeloma

Watch Amy tell her story »As a healthy and active 37-year-old, my world shattered when I was diagnosed with an incurable blood and bone marrow cancer, multiple myeloma. This rare cancer tends to be found in men aged 70 and over, so my situation was met with puzzled doctors and a poor prognosis.

Myeloma creates holes in your bones, which has caused extraordinarily painful fractures in my spine, skull, pelvis and ribs. It is debilitating. I even had to learn to walk again when my spine collapsed. In order to afford healthcare, I continued to work full-time for many years, until last year, when I had to take disability as my work could not accommodate my treatment and fatigue-impacted schedule. Along the way, there were times when I just could not make it to work due to fatigue, feeling ill and pain. My cancer has also had a severe impact on my stamina and ability to have a social or family life—again from the fatigue, nausea and pain.

Not only am I fighting a rare cancer, but I am also forced to deal with challenging policies, red tape and delays from insurance companies. Two stressful and dangerous insurance policies are pre-authorization and formulary restrictions. Formulary restrictions sometimes stop my insurance from covering the cost of the medications I have been relying on; pre-authorization can slow access to my medication, since new and/or additional specialists have to authorize my urgently needed drugs. Both of these policies have slowed my healing and possibly shortened my life expectancy by allowing my cancer more time to progress. They also end up costing the insurance company more money in the long run, as delays mean getting sicker, then having to battle back an even higher cancer load and thus needing even more medications to “dig out of the hole.”

From the time I started treatment in 2008, I have been working with several doctors to determine the exact medication combination that is the most effective and tolerable. Sometimes my treatment has been oral chemotherapy, which can severely disrupt the balance of one’s stomach. Unfortunately, after determining a workable medication combination that allows me to function at a semi-decent level, my insurance sometimes changes its formulary restrictions. They decide to no longer cover the cost of my medications and shift the brunt of the costs onto me. When I could not pay these enormous fees, the insurance company would propose other medications that were different enough to throw off my medication regimen, which could mean ineffective chemotherapy. Some insurance substitutions were so dangerous for me that my doctor would not even allow me to take the substitution. So, I then must start all over again, all the while losing time in battling my cancer.

My health is always in a precarious state as insurance companies fail to look at the big picture—they often use tactics such as formulary changes to lower their bills at the expense of patients like myself. The medication swaps that insurance companies suggest interact with my body and chemotherapy in a different way than my original prescription, and I need a specific combination of drugs to keep me functioning. Needing my precise original prescriptions, I have had to appeal and fight to keep my drugs and health. Both the appeals process and pre-authorization continue to get in the way of my healing and quality of life, including my ability to work. Appeals take countless hours from very sick patients who often do not have the stamina to fight. And, sadly, doctors are often not allowed to dispense medications they know could help because of the slow pre-authorization process. These obstacles have delayed my treatments too many times, which only shortens my days.

As with most cancers, myeloma begins to evade treatments, causing urgent searches for new ones. I have gone through most FDA-approved treatments for my cancer, so the only hope for extending my life is successful medication developed in clinical trials. I, and my loved ones, participate in Cycle for Survival, where I have personally raised $90,000+ that goes directly to clinical trials for rare cancer. When I am not participating in these events, I am also advocating for better healthcare laws that serve and protect patients. At the end of the day, my life is hinged on these protective healthcare laws and medical trials, and I contribute so that others never have to go through what I have gone through.

Pre-authorization fact sheet infographic

For patients: What Is Pre-Authorization? fact sheet

An insurance company may require a patient to get its approval before it agrees to cover the cost of a prescribed drug. This is known as pre-authorization or prior authorization (PA). Learn more about pre-authorization and how it might affect care. View our fact sheet >>

Common UM Practices & Consequences

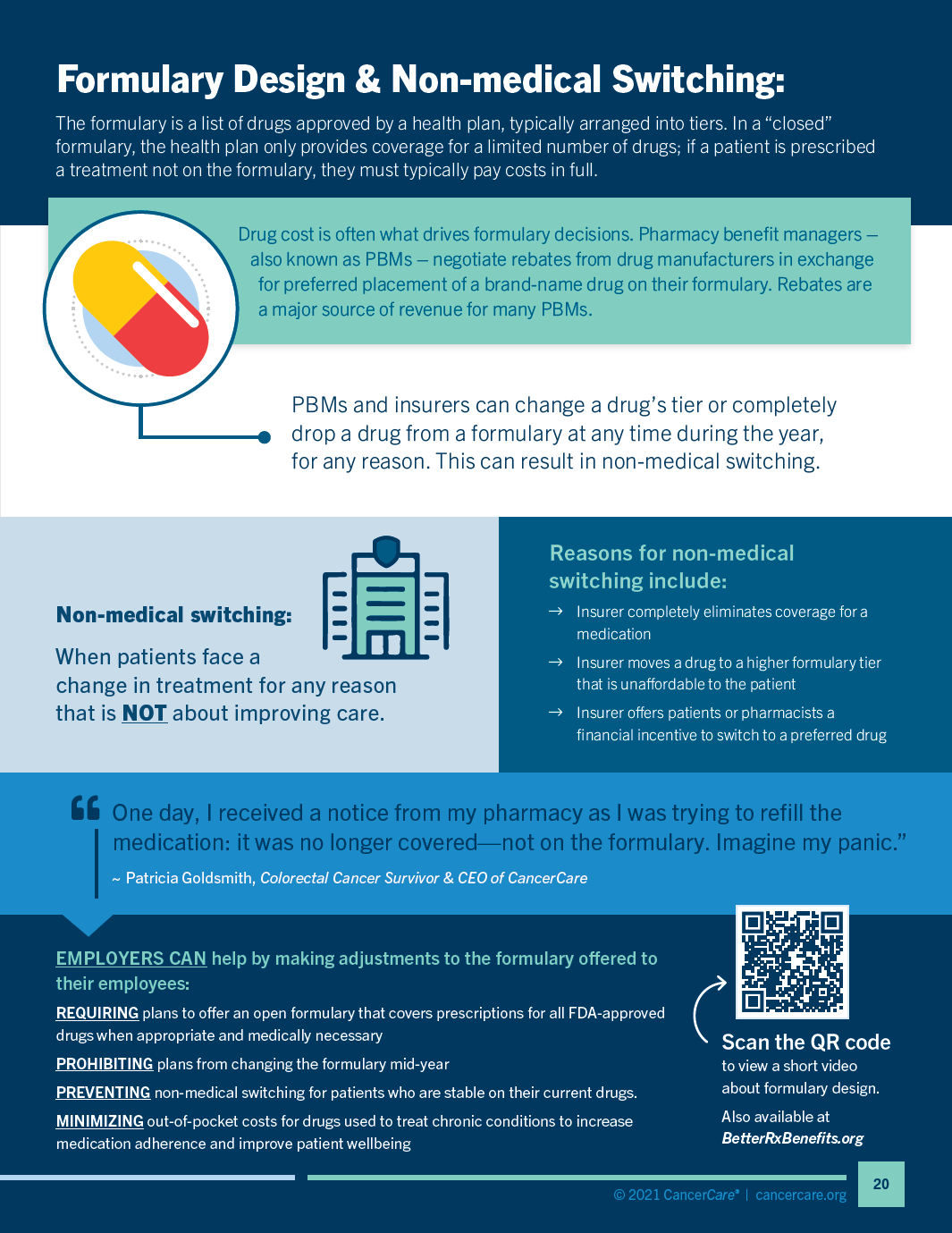

Formulary Design

How do formularies work?

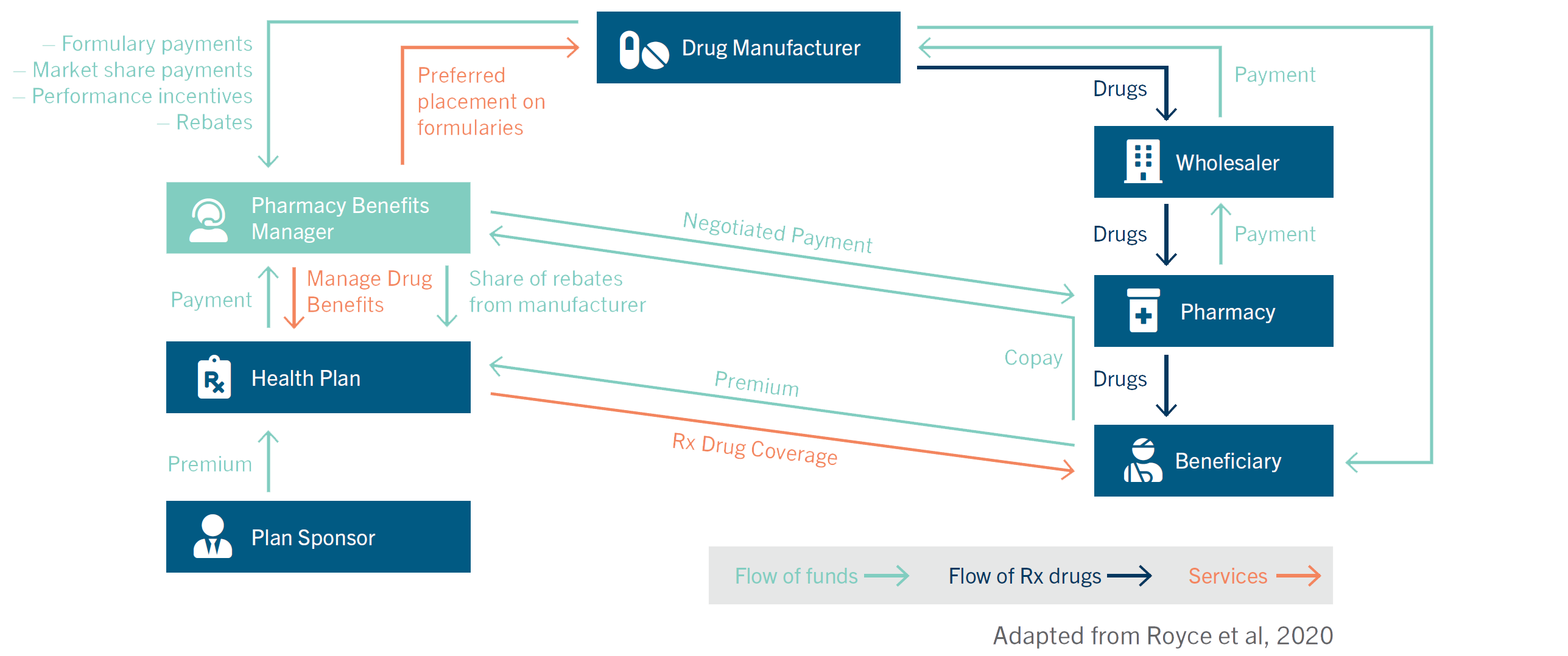

A formulary is a list of available drugs approved for use by a health plan. It is typically divided into tiers, which reflect the level of cost sharing required each time the prescription is filled—that is, how much of the drug’s price a patient will need to cover at the pharmacy counter as determined by their copay or coinsurance rate. The formulary is designed by insurers and pharmacy benefit managers (PBMs), who presumably examine the clinical outcomes associated with different medications and current treatment standards.38 Drug costs also play a significant role in formulary design, including rebate “paybacks” negotiated with drug manufacturers that generate profits for PBMs, but don’t necessarily lower costs for patients. It’s nearly impossible to determine the basis for a formulary design because there is no transparency in the process; there is no requirement that PBMs disclose how decisions are made, or how or when changes are made.

Formularies can be open, restrictive or a mix of the two. An “open” formulary provides at least partial coverage for nearly all drugs, even if they’re not included on the preferred list. In a restrictive or “closed” formulary, the health plan only provides coverage for the limited number of drugs. If a prescribed treatment is not on its formulary, the insurer is unlikely to provide coverage and patients must pay costs in full.

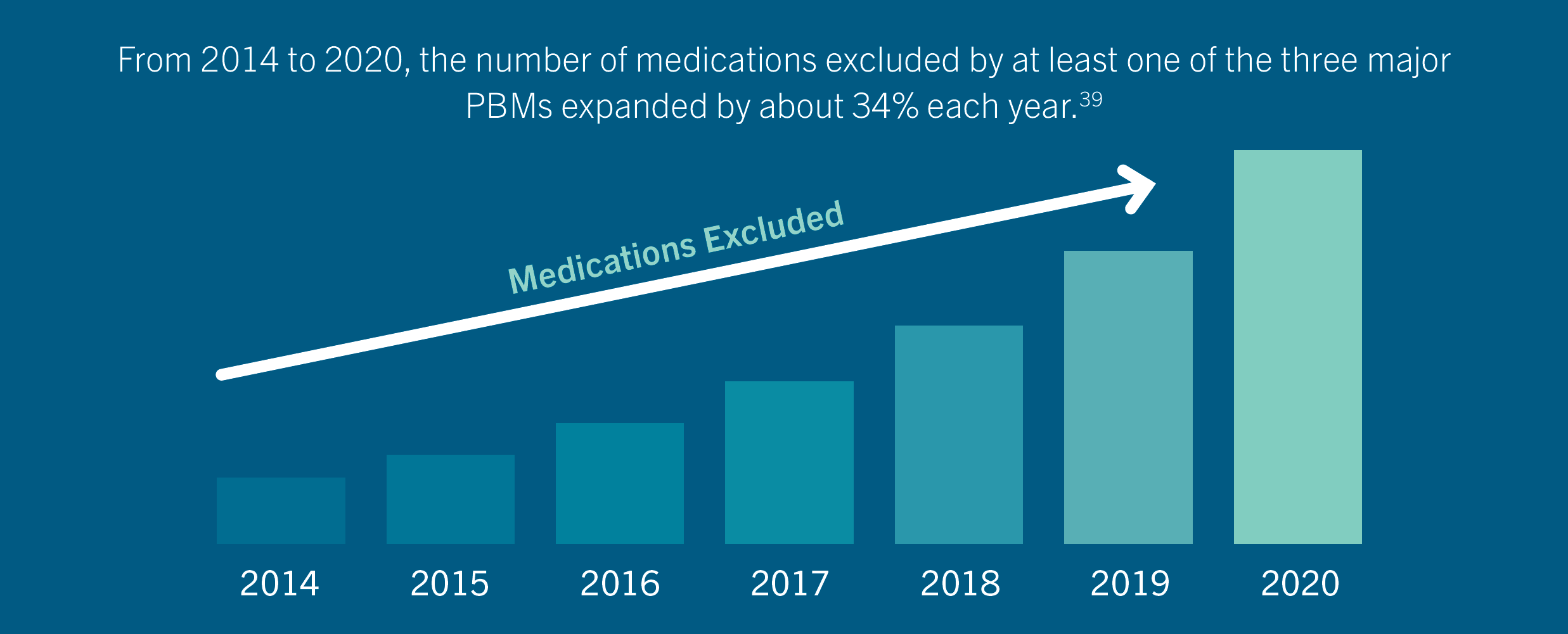

From 2014 to 2020, the number of medications excluded by at least one of the three major PBMs expanded by about 34% each year. In other words, patients are increasingly likely to discover “gaps” in their drug benefits and face significant out-of-pocket costs if they need to access a medication that is not on the formulary.39 While restrictive formularies have become a common UM tool, multiple studies have linked their use to increased medical costs and higher total healthcare spending.15 In contrast, studies of open formularies suggest better outcomes. For example, researchers modeled scenarios under different formulary structures for patients with HIV and found that all major outcomes, including survival rates and overall treatment costs, were significantly better in the open formulary scenarios.40

How are formulary tiers set?

PBMs set formulary tiers based on a drug’s approved use, (presumably) its efficacy and benefits, cost to patients, cost to the insurance company and cash-back rebates that manufacturers pay the PBM. Formularies include both brand-name drugs and generics—versions of brand-name drugs that sell at a lower cost, but have the same active ingredients, dosage, strength, safety, effectiveness and quality. Generally, generics and low-cost drugs appear in lower tiers, with brand-name treatments appearing in the higher tiers.

Tier / Drug Type Description Cost 1 | Lowest Copay

Usually GenericMost generic prescription drugs. Lowest copayment. $ 2 | Medium Copay

Usually Preferred Brand-Name DrugsA PBM may give a drug preferred placement because it has negotiated cost-saving rebates from the manufacturer, in exchange for placement on a lower tier that drives a higher volume of use. These rebates are typically not passed along to the patient or employer. $$ 3 | High Copay

Brand-NameSome of these brand-name drugs may have lower-priced generics on Tier 1 or 2. $$$ 4 | Highest Copay

SpecialtyDrugs used for chronic and serious illnesses, including cancer.

Instead of a flat copay, patients may be required to pay a percentage of a drug's total cost, which is called co-insurance.

Alternatively, some employers designated Tier 4 for preventative care and remove any cost-sharing requirements.$$$$ Typically, PBMs and insurers prefer that physicians prescribe Tier 1 medications as a first step, versus a more expensive brand-name drug from Tier 2 or 3. However, this isn’t always the case: some PBMs receive and pocket high-volume rebates for brand-name drugs in exchange for lower tier placement, so the brand-names may end up costing patients less than the comparable generics.

Prescriptions for drugs that are not on formulary are usually denied coverage; patients need to pay the full cost or appeal to the insurer to include the drug, a time-consuming process that typically delays treatment and adds stress. Formularies vary by health plan and change over time, often without any transparency or notice to patients or clinicians. The same drug might be Tier 2 under one health plan and Tier 3 under another, or a drug’s tier position may change when a health plan changes its formulary.

The role of rebates

PBMs negotiate rebates from drug manufacturers in exchange for preferred placement of a brand-name drug on their formulary. Rebates are refunds that are paid to the pharmacy benefit manager by the drug manufacturer after the drug is sold—so the PBM’s final net price for the drug is lower than the original list price. PBMs may pass the rebates on to health plans; however, their contracts often allow them to keep a portion. Rebates are a major source of revenue for many PBMs.

Mark Peters, PharmD, Vice President of New Business Development & Outreach at CancerCare, explains how rebates drive drug placement on formularies. “Some drugs have such large rebates that it’s very difficult for newer drugs in their class to get placed in the same formulary tier.” The new drug typically ends up placed at a higher tier rate, if it’s covered at all. “The PBM doesn’t want patients to use the new drug even if it’s a better remedy for them, because the rebates make the older drug so profitable.”

Because rebate negotiations are not made public (in fact, they’re a closely guarded secret), it’s difficult to gauge if or how savings are passed on to patients or the employers who sponsor plans. Studies suggest the direct benefits to patients may be minimal. For example, a 2021 study found that changes in net drug prices—which reflect the savings to PBMs, post-rebate—were not correlated with changes in patient out-of-pocket spending. These studies concluded that rebates reduce PBM spending on drugs but aren’t directly passed on to patients.41 To address this, some policymakers have called for an end to confidential rebate negotiations; others propose a process that would apply rebates directly to the patient’s out-of-pocket cost when they pay for drugs.41

Generics, biosimilars & competitive pricing

The competitive advantage conferred by rebates has confounded conventional wisdom about brand-name vs. generic drug or biosimilar pricing. As described above, generic drugs are slight variations of a brand-name drug, marketed at a lower cost. Likewise, a biosimilar is a lower-priced alternative to a biologic drug (therapies developed from living cells that help boost the immune system’s response).

Generics and biosimilars are intended to keep brand-name drug prices in check. In 1984, the Hatch-Waxman Act made it legal to promote price competition via generics once a brand-name drug’s patent protection runs out. The FDA has created a similar pathway to approval for biosimilar drugs.

The rebate system, however, has turned the tables and distorted the market. For many years, insurers and PBMs steered patients towards generic or biosimilar options through their formulary tiers. Now, large PBMs are altogether excluding some generics and biosimilars from their formularies, despite their being effective and available at lower list prices, in favor of brand-name drugs that supply significant rebates.

For example, Express Scripts, a PBM that handles benefits for 100 million Americans, gave preference to nine brand-name drugs and excluded their generics in a 2019 formulary change.

The excluded generics included an insulin that was half the price of the brand-name and an asthma medication priced at a 70% discount to the brand-name price.42,43

The fact that savings from generics weren’t appealing to this cost-focused PBM hints at the high profits it makes from brand-name rebates. Again, these savings are not necessarily passed on to patients; the rebate process and resulting exclusions effectively block patients from accessing the cheaper generic medicines because, to patients, they actually cost more out-of-pocket than the brand-name drugs.

In cancer care, oral drug treatments have rapidly joined chemotherapy and biologic infusions as safe and effective cancer treatments. These drugs are usually covered as a pharmacy benefit, while infusion therapies typically fall under medical benefits. While the oral drugs offer numerous benefits, they often cost patients much more to access, due to the cost-sharing requirements in restrictive formulary designs. Proposed “oral parity” legislation (such as the Cancer Drug Parity Act of 2019) seeks to make oral medications as accessible to patients as infusions and remove barriers that health plans might implement to limit their use. This legislation requires a plan to cover self-administered anticancer medication at a cost no less favorable than the cost of IV, port-administered or injected anticancer medications. Parity laws have found major support among state governments. Especially important during the COVID-19 pandemic, oral therapies have allowed many patients to stay at home and avoid the potential virus exposure from in-person chemotherapy infusions. Oral therapies can also minimize the need for transportation and time off from work, thereby supporting increased productivity.

Mid-year formulary changes & non-medical switching

Formulary plans can change mid-year or at any other time, which leaves the insured, who often can only choose their health plan during open enrollment, with an unexpected cost or lack of access to treatments. Changes may reflect treatment advances or new findings, but changes also occur when PBMs negotiate lucrative new deals with drug manufacturers. Depending on negotiations, a treatment might replace another, receive a better tier placement or be eliminated entirely from a plan’s approved formulary. Many states and patients-rights advocates are fighting to prohibit arbitrary and unexpected formulary changes.44

Changes to formulary coverage can result in non-medical switching, which occurs when changes are made in a patient’s treatment plan that are NOT prescribed by their doctor for medical reasons. For instance, non-medical switching can occur when an insurer completely eliminates coverage for a medication, moves a drug to a higher formulary tier that is unaffordable to the patient, or offers patients or pharmacists a financial incentive to switch to a preferred drug.

A 2021 promotion from Cigna illustrates the last case: the insurer removed a widely used psoriasis drug from most of its formularies then offered patients a $500 debit card for agreeing to switch to a different medication.

While Cigna framed the change as a cost-saving benefit to patients, physicians and advocacy groups decried the offer as “unethical,” “unconscionable” and “coercive” for “targeting patients and enticing them with a financial incentive, particularly during a pandemic, when finances and employment for many are uncertain.” They expressed concern that the move would disrupt long-standing relationships between physicians and patients and could jeopardize patient health if the new medication was not as safe and effective as the replaced drug.45

It often takes doctors and patients months, or even years, to find the most effective medications to manage a patient’s cancer or other serious illness. When an employee loses access to a medication that has stabilized their condition, they can experience re-emerging symptoms, negative side effects or even a relapse of their illness. For patients using biologic and biosimilar cancer therapies that are precisely tailored to the genetics of their cancer, a switch in treatments can be especially precarious. This can also be the case for certain “quality of life” medications that don’t treat cancer, but rather treat medication side effects (like nausea) or long-term post-surgical effects.

While formulary changes and non-medical switches are intended to reduce costs for a health plan, costs may actually increase over time from extra administrative work, more doctor appointments, additional laboratory work and more hospitalizations due to adverse effects and treatment failures.46,47 Formulary changes can also create higher out-of-pocket costs for patients, decreased work productivity and increased stress and anxiety. While some patients can make a more affordable switch, others may not have access to acceptable alternative medications and may abandon treatment altogether.

Case study: Non-medical switching, Patricia Goldsmith

Patricia Goldsmith

Patricia Goldsmith

New York, New York

Colorectal cancer

Watch Patricia tell her story »In 2014, out of the blue, I was diagnosed with colorectal cancer. I was really lucky; I had great insurance, I had contacts at every cancer center in the country and my case was handled properly. But unfortunately, one of the consequences of my treatment was a very, very bad side effect: major gastrointestinal distress. And that can have a dramatic impact on anyone’s life. Thankfully, my physician prescribed a medication that worked. As time went on, we eventually determined a dosage that worked very effectively for me. It was a lower dosage than when I originally started on the drug; life was all good and I could continue my daily activities.

One day, I received a notice from my pharmacy as I was trying to refill the medication: it was no longer covered—not on the formulary. Imagine my panic. I was fortunate enough that I had some stockpiled because the dosage had been reduced. My surgeon, my primary care physician, everyone went through all the appeals processes and United Healthcare / OptumRx said, “No.” So, my primary care physician suggested, “Trish, why don’t you just try what they’re substituting and see if it works. Try it for a month.” I agreed and went to the local Walgreens drive-thru to pick it up. I pulled up and the pharmacist said, “I’m sorry, you’re going to have to come inside, it’s too big to put in the drawer.” So I walked into the store and picked up a rather large box.

It was slightly smaller than a breadbox. Inside were 180 small packets. The directions were to take six packets each day, mixing each individual packet with eight ounces of juice or water. The packets couldn’t be combined. This was not a regimen I could tolerate. Immensely frustrated trying to reach someone at OptumRx, I finally got a human being on the phone line. I said, “You have got to be kidding me about this.” And here’s the solution that was offered: “Well, you can mix the packet in applesauce.”

It was slightly smaller than a breadbox. Inside were 180 small packets. The directions were to take six packets each day, mixing each individual packet with eight ounces of juice or water. The packets couldn’t be combined. This was not a regimen I could tolerate. Immensely frustrated trying to reach someone at OptumRx, I finally got a human being on the phone line. I said, “You have got to be kidding me about this.” And here’s the solution that was offered: “Well, you can mix the packet in applesauce.”Needless to say, this was not an acceptable option for me. I am a busy person and I didn’t have the time or patience to mix this medicine six times a day. Instead, I decided to take the original medication, which cost me $695 out of pocket per month. Then, about a year and a half ago, I got notification from OptumRx that my original medication was back on the formulary and that I could get it through mail order. My copay was about $60 a month, they would send three months’ worth and I thought, “This is great!”

I waited two or three weeks and heard nothing. Then I got a letter that this medication was out of stock, but they had a substitute for me. Can you guess? The packets again. I went to my local Walgreens and asked my pharmacist if there was a shortage of my medication or a problem keeping it in stock. She said, “No, I have it in stock.” So I figured it’s just OptumRx’s way of trying to switch me to the less-expensive treatment.

I still take the medication. If I run out, I’m back to the six-packets-a-day plan or the $695-a-month plan.

Formulary design & non-medical switching fact sheet infographic

Formulary design & value assessments

In recent years, PBMs have increasingly used value assessment frameworks to inform drug formulary design and their negotiations with drug manufacturers. Value assessments are economic frameworks applied to healthcare decisions to determine whether the benefits of a drug or treatment are worth the price being charged for it. Each framework comprises a number of factors, including efficacy, cost, benefits, risks and, sometimes, the larger impact on a group or society.48

Value assessments are typically designed to average and summarize; this makes it challenging to apply them to individual needs and fails to acknowledge diverse circumstances among patients. As health economist Lisa Kennedy points out, current frameworks “aren’t reliable across the same patients over time, across different patients and, additionally, fall down when required to measure more difficult things such as [treatment value] in the elderly or the very young.”49 In addition, the formulas used to make these assessments aren’t always transparent.

While framework design involves multiple stakeholders, patients are notably missing among them. Most value assessments fail to incorporate the diverse and dynamic ways patients think about value—for instance, the cancer patients who value treatments that will allow them to get back to work faster, return to exercising or playing piano, or to attend a grandchild’s graduation.

ICER & concerns regarding value assessments

An influential but controversial agent in value assessment is The Institute for Clinical and Economic Review (ICER), a private research organization, and its framework, the “incremental cost-effectiveness ratio.” While this framework has gained traction among insurers and PBMs, CancerCare and many leading medical organizations have criticized ICER’s methodology, citing its discriminatory “one-size-fits-all” models, lack of transparency and failure to incorporate real-world perspectives from patients, caregivers and physicians.50

ICER only discloses the details of their assessment models to select stakeholders. This “black box” process makes it impossible for researchers to share methods, conduct peer reviews or attempt to replicate and validate results. The lack of transparency also hides the model’s underlying assumptions, limitations and gaps that can impact the relevance of its results for patients with even slightly different profiles.

Without patient input, crucial perspectives on “value” are missing from ICER’s assessments. Value Our Health, a consortium of leading healthcare organizations, argues that ICER reduces the meaning of “value” to “cost-effective” only. The National Health Council’s Patient-Centered Value Model Rubric outlines the need for patient involvement at every stage of the value assessment process, from initial development to the sharing of results. Value assessments should consider multiple facets of patients’ lives and broader societal perspectives, such as a patient’s ability to work and caregiver burden.51,52

QALYs (Quality-Adjusted Life Year)

A primary concern regarding ICER is its use of a QALY standard in its value assessments. QALY stands for “Quality-Adjusted Life Year” and is an older economic tool used to quantify the net value of a treatment by determining how its cost corresponds to the potential benefit. The QALY model essentially creates a formula for “quality of life x length of life” that can be stated as a single number.

In the ICER framework, one QALY is defined as one full year of perfect health and valued at roughly $100,000 to $150,000.

ICER calculates a treatment’s “cost-per-QALY” and compares it against that $100,000-$150,000 threshold. Healthcare experts point out that this is “an artificial affordability threshold,”51 but one with very real consequences for patients when it’s applied by insurers and PBMs. For example, in 2018 CVS Caremark announced plans to adopt ICER frameworks for managing their drug formulary and would no longer cover drugs with a cost-per-QALY over $100,000. Consider the real people who would be denied medication because it is deemed that the value of their lives is capped at $100,000 a year. Their family would no doubt say that another year with their loved one is priceless.

By design, the QALY’s narrow focus on “perfect health” devalues and discriminates against people due to their age, disabilities or chronic conditions. How these patients actually view their quality of life is not considered. For the many individuals who never meet the criteria for “perfect health,” ICER’s calculation credits them with only a percentage of a life-year. This makes it even harder to show a treatment is a “valuable” investment according to the QALY threshold. When QALYs are used to determine cost effectiveness for a drug formulary or other health plan coverage, the resulting decisions have the same discriminatory flaws and could lead policymakers and payers to conclude that certain treatments for seniors, patients with chronic conditions or people with disabilities are not worth covering.

The Affordable Care Act bans the use of QALYs for creating Medicare drug formularies, building on similar prohibitions and civil rights protections established earlier through the Rehabilitation Act and Americans with Disabilities Act. As Patricia Goldsmith, Chief Executive Officer of CancerCare, noted, “The Medicare program has long barred the use of QALYs in reimbursement and coverage decisions, recognizing that this metric discriminates against people with cancer and other serious health conditions. It’s frustrating that state and federal policymakers continue to debate their use in public programs. Organizations representing millions of patients and people with disabilities demonstrate a united front against state and federal policies that use the QALY metric or import it through reference pricing.”

Case study: QALY-based value assessments, Chris & Michelle Bushell

Chris & Michelle Bushell

Chris & Michelle Bushell

Calgary, Alberta, Canada

Cystic fibrosisWe are the parents of two sons afflicted with cystic fibrosis (CF), the most common fatal genetic condition. From the moment Zachary (age 19) and Brett (age 16) arrived in this world, we have never known for certain what tomorrow would bring, when the next 2:00 a.m. trip to Emergency Care would occur, or whether hours of chest therapy would reduce the discomfort of constant rasping and wheezing. For 19 years, we’ve lived daily with the prospect of potentially losing one, if not both, of our sons.

Now imagine knowing that a life-saving drug is available for CF patients. Trikafta has changed the lives and long-term outlook for CF patients worldwide. It’s the silver bullet that can slay the CF monster and provide a chance at a normal life. Trikafta is approved for use and covered by insurance in most countries in the western hemisphere—except for our home country of Canada.

This devastating reality is due to the use of QALY-based value assessments in Canada’s public health system, which fail to account for life-changing innovations, precision medicines and other high-cost specialty drugs. The review process is also excruciatingly slow: it took nearly five years from Health Canada approval for Trikafta’s predecessor to gain public healthcare coverage!

Time is not on our side. These drugs are preventative: excessive delay or imposing funding conditions, such as patients needing to have low lung function, defeats the purpose of the drug and is inhumane. CF eats away at patients’ lungs each and every day.

A few weeks before Christmas 2020, our oldest son, Zach, was hospitalized. He had been plagued with an unresponsive, highly resistant gram-negative bacteria for the past five years. During that time, he used colistin (the “antibiotic of last resort”) twice daily, converting an IV med into an inhalant to reduce the threat of this deadly bacteria. His lung function had dropped to just 40%. We thought the moment we had dreaded since his birth had arrived: CF was finally going to win.

We were determined to get Trikafta for Zach no matter what. A clinic in the U.S. took the generous step of granting a virtual assessment and prescribed Trikafta on the condition that Zach was “in the process of moving” to the United States. Shortly afterwards, we took the COVID risk and flew to the United States for Zach’s first month’s supply.

Three weeks later, after starting Trikafta, Zach’s lung function was 71% and his CF team in Calgary stopped his antibiotics. As parents that have been expecting the early death of a child, the feelings we had seeing those results were nothing less than euphoric. Today, Zach’s lung function continues to climb and the resistant bacteria that had plagued him are gone. He’s gaining weight and the abdominal pain he’s suffered his whole life is gone.

Trikafta (or its successor) is a drug that Zach will have to be on for the rest of his life. The reality is that, in order to keep receiving it and the care he needs, we’ve had to send Zach to live in the United States. Zach has a U.S. passport; he was born in California while we were working there as expats. But he grew up in Canada; our family is Canadian. As Canadians, we’re still anxiously waiting for Trikafta to be available to our younger son, Brett. It’s painful to see our boys separated not only by miles, but by the opportunity for a healthier life. We’ve agreed to share this private part of our lives because we feel obligated and determined to help Brett and other Canadian CF patients.

QALY-based value assessments fact sheet infographic

Common UM Practices & Consequences

Step Therapy

What is step therapy?

Step therapy, sometimes referred to as a “fail-first” protocol, requires patients to use treatments on lower formulary tiers (usually generics or preferred drugs that provide cost-savings to the insurer or larger rebates to the PBM) before being approved for drugs in higher tiers or, in some cases, drugs not included in the formulary. Patients and their physicians must demonstrate that the required treatment has “failed” before the insurer will authorize coverage for the treatment originally prescribed.

The step therapy approach is intended to address the rapidly rising costs of healthcare by lowering or maintaining costs for the insurer and the patient. “Lower costs” may only apply to the PBM and insurer, however; for patients, step therapy can mean added out-of-pocket expenses, as well as significant burdens on their time and well-being.

Concerns regarding step therapy

Concerns regarding step therapy

While encouraging the use of generic or lower-cost alternatives may sound positive, step therapy is a flawed system that can put patients at risk. Some insurers even require patients to “re-try” drugs that already failed or worsened their condition in the past. As health policy expert Robert Popovian, PharmD, MS, notes, “There is no empirical evidence that step therapy reduces overall healthcare costs and [offers] improvements in patient outcomes short or long term. Insurers or PBMs and their clinical staff have never explained what it means to fail. Should a patient suffer from worsening disease symptoms or side effects, or maybe be hospitalized? Insurers and PBMs also unnecessarily demand that providers justify every single intervention they utilize, through mounds of paperwork.”53Delayed, disrupted and denied treatment due to step therapy causes serious harm in the time-sensitive fight against cancer and other aggressive diseases. It can also cause serious side effects and major setbacks in managing chronic illnesses, as well as significant impacts on employee productivity and presenteeism.

For example, Virginia Maxwell and her son have pityriasis rubra pilaris (PRP), an auto-immune disorder that causes inflammation and scaling of the skin, which can lead to bleeding sores and infection. While Virginia can successfully manage her PRP with an injectable drug, the family’s health plan required her son to try other treatments first before he, too, could be approved for the injectable medication. This approach resulted in a deteriorating condition so severe that he missed school and suffered extreme pain and discomfort.54

Expensive cancer drugs are often targets of step therapy. Yet many oncology drugs do not have substitutes that are both equally effective and less costly. When cancer patients don’t get the right drug at the right time, the length of illness can increase.55 One study found that breast cancer patients who endured a three-month or more delay in treatment had a 12% lower five-year survival rate. The uncertain process of waiting for lesser drugs to fail can take weeks or months. Additionally, step therapy has been shown to reduce the long-term effectiveness of treatment.56

Advances in treatment may outpace coverage decisions, putting step therapy out of sync with best practices.

For example, in 2019 the FDA approved a new first-line treatment for patients with advanced renal cell carcinoma.

Many step therapy protocols, however, still require an older drug be tried first, based on outdated guidelines—even though updated research indicates far better outcomes with the newer medication.

The true cost of “saving” money

Studies show that the money insurers save through step therapy comes at the expense of patients’ health and financial well-being.

The step therapy process pushes some patients to abandon beneficial drug treatment. A 2009 study looked at patients with bipolar disorder who were required by insurance to use pre-authorized drugs in place of the medications prescribed by their clinicians. Initially, the use of the pre-authorized drugs showed a cost savings to the health plan. But a closer look at the data revealed the “savings” corresponded to patients who stopped treatment altogether when faced with a different medication than what their doctor prescribed.57

Step therapy can also create unexpected out-of-pocket costs for patients, since they are required to pay a copay for the pre-authorized drug and then another copay once the drug preferred by their doctor is finally approved. In addition, some plans require the use of brand-name drugs that are on a formulary’s lower tiers due to the bigger rebates their manufacturers offer. While PBMs and insurers profit from these rebates, patients in high deductible plans may end up burdened with the full out-of-pocket costs associated with a brand-name drug’s higher price. It’s well known that higher out-of-pocket costs are associated with increased rates of treatment abandonment.

The use of step therapy can also result in loss of income, lost time at work or in school and other social and economic burdens. One study looked at data from employers who implemented step therapy and compared it to employers who did not, to understand the effects of step therapy on patients taking antihypertensive drugs. Initial results showed a reduction in costs from the step therapy group; over time, however, there was a marked increase in those patients’ healthcare costs, due to hospital and emergency room visits. In other words, step therapy may create barriers to effective care, which ultimately results in worsening health and higher treatment costs, as well as presenteeism and reduced productivity.

The practice of step therapy has been condemned by the American Medical Association, the American Society of Clinical Oncology and other leading medical organizations.

Critics argue that step therapy prevents doctors from making treatment decisions based on clinical information and puts centralized cost-saving policies ahead of patients’ specific needs. Others note that step therapy takes too narrow a view of what constitutes “cost,” ignoring long-term costs for care and the physical and emotional costs levied on patients.

The proposed Safe Step Act would place federal restrictions on step therapy and create a streamlined process for patients and their healthcare providers to request exceptions. Among its restrictions, the Act would protect patients from having to re-try treatments that previously failed or try new treatments when a prescribed drug has stabilized their condition. As of August 2021, 29 states have already passed laws limiting or regulating step therapy.

Case study: Step therapy, Justin Williams

Justin Williams

Justin Williams

Atlanta, Georgia

Polymyocitis

Watch Justin tell his story »In 2015, I was an average 28-year-old until I woke up on my bathroom floor after passing out unexpectedly. That moment changed the course of my life. I scheduled a doctor’s appointment, where several tests were run that ultimately led to my diagnosis of polymyositis, an inflammatory disease that causes severe muscle weakness.

The tests showed extremely high levels of creatine kinase (ck)—my number was off the charts. For reference, my test said my levels was 6752 when the average levels are between 24.0 - 204U/L. High levels of creatine kinase indicate muscle deterioration. My doctor was thrilled that I had come in so quickly after experiencing my symptoms so we could attack the disease immediately. Other symptoms had shown themselves that I wasn’t so quick to notice: I couldn’t lift things over my head, I couldn’t do push-ups, I was barely able to get myself out of bed and I was having trouble swallowing liquids and most food.

Immediately upon my diagnosis, my doctor knew what to prescribe: a rituximab infusion. The infusion would only have to be done once every two years and would significantly reduce my ck levels. I have health insurance through my employer, but they denied the claim. The insurance has a step therapy policy that forces patients to try less effective, cheaper medication before the pricier, effective drug.

I was prescribed the next best option, prednisone. In addition to the prednisone, I was put on seven other medications to balance out the intense side effects caused. My face swelled up, my body was so inflamed that I couldn’t sleep for more than two hours a night, and I became extremely irritable. My job was in jeopardy because I was so unlike myself. I couldn’t think clearly and had to cut my workload. I was like a zombie.

After about six months of hardly sleeping and dealing with these difficult side effects, it got to a point where I was crumbling. There was one day when I found myself suffering from shortness of breath and felt a panic attack coming on. This drove me to check into the hospital for a second time, where the doctor said I had what is known as “athlete heart syndrome”. This is when the heart never really has a chance to rest; it’s always working at full capacity. It’s extremely dangerous and can contribute to further issues down the line.

It was clear the prednisone wasn’t working. I started out on a high dosage of the prednisone, but extensive time on a high dose will cause other issues. Over time, I dropped to 10 mg with little success in my levels and several other health challenges. At this point, my healthcare team requested my insurance to cover the infusion once again. They finally approved it after months of suffering.

Upon my first infusion of rituximab, my ck levels started to drop significantly. It wasn’t until about four to five months later that I began to feel relief from my symptoms. I’m now at the lowest creatine levels I’ve seen: 484. I have continued to get the infusion every two years and it has helped. I only wish I never had to go through the step therapy process at the beginning; that was one of the most challenging times of my life. Thankfully my mother, Gabrielle Jones, was by my side and fighting along with me every step of the way.

Step therapy fact sheet infographic

Case study: Step therapy, Heidi Barrett

Heidi Barrett

Heidi Barrett

Everett, Washington

Psoriatic arthritisI suffer from psoriatic arthritis. I also have five children and a husband, all of whom have at least one auto-immune disease. Our family receives health insurance through my husband’s employer and I only recently have been able to return back to work, which was critical due to the rising cost of my family’s medical care. I am a family law paralegal.

All of our family members who suffer from this disease had been on a medication we found successful: Remicade. It falls under a class of drugs called “biologics.” We sort of have a “science experiment” going on within our family, where one person tries a medication, finds success, and the others follow suit. Without this drug, my family would be in wheelchairs from our pain and may not even be alive.

The insurance provider denied the medication, despite the knowledge that it would help me. Enforcing a policy called step therapy, the insurance company forced me to try other, cheaper medications first. If those medications “fail,” the insurance company will then approve the more expensive, effective medication. Of course, these medications do fail and it results in extra hospital visits, vomiting, pneumonia and strep throat while the patient is on them. Eventually, I received approval for Remicade and reached a point where I had worked my way up to a high dose, which had been truly helpful for me.

Out of nowhere, our health insurance decided they no longer wanted to pay for this life-saving medication and pulled it out from under me, citing expenses. They said I could restart the Remicade at a low dose, as part of step therapy. That was not an option for me because biologics like Remicade can cause life-threatening drug interactions if they are reintroduced at a low dosage. It’s extremely dangerous and not recommended. Our hands were tied.

My only option was switching to a drug called Simponi, which is about 80% as effective as Remicade. This turned out to be the lesser of two evils, so we had to move forward with it. Unfortunately, my dose wasn’t enough to compensate for my symptoms, and if I were to get the infusion as frequently as needed to compensate for the reduced efficacy, it would cost $6,000 out of pocket each time. I was in so much pain when I first switched to Simponi that I barely left the house and even had to use a cane for about six months. Had our insurance decided to continue my care and cover the high dose of Remicade, I could have avoided this severe pain and suffering.

Step therapy, while there may be a time and place for it, really isn’t beneficial to those of us who are hurting and need specific medications to live daily life. Doctors, administrators and pharmacists who have no experience treating specific diseases are calling the shots and determining the pre-authorizations required for certain medications. We need specialized experts determining what medications are best for treating our individual cases.

Not only have we had to deal with bankruptcy due to the restrictions in our health insurance plan, but step therapy has caused additional, unnecessary painful days for our family and has put us in life-or-death situations. I only fear what will happen to my younger children when they turn 26 and have to navigate these scary insurance policies on their own.

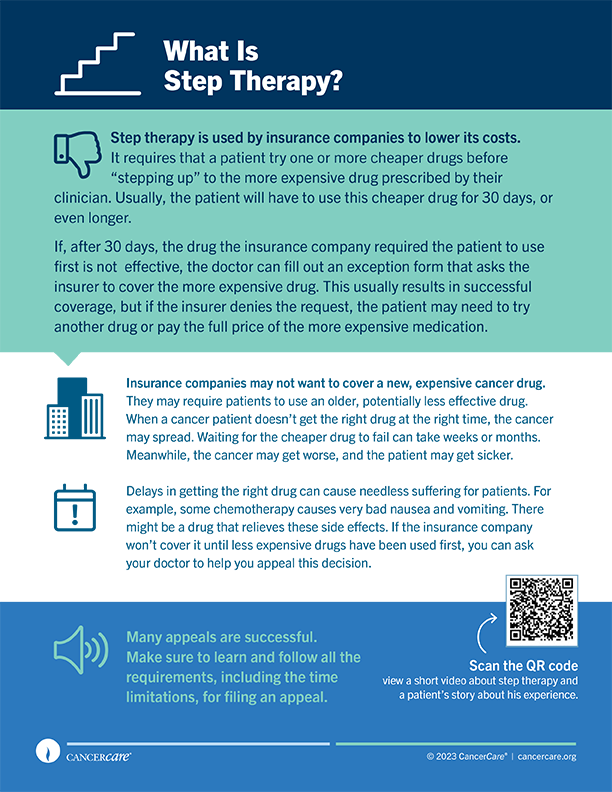

For patients: What Is Step Therapy? fact sheet

Step therapy is used by insurance companies to lower its costs. It requires that a patient try one or more cheaper drugs before “stepping up” to the more expensive drug prescribed by their clinician. Learn more about step therapy and tips to get the optimal coverage. View our fact sheet >>

Common UM Practices & Consequences

Specialty Pharmacies

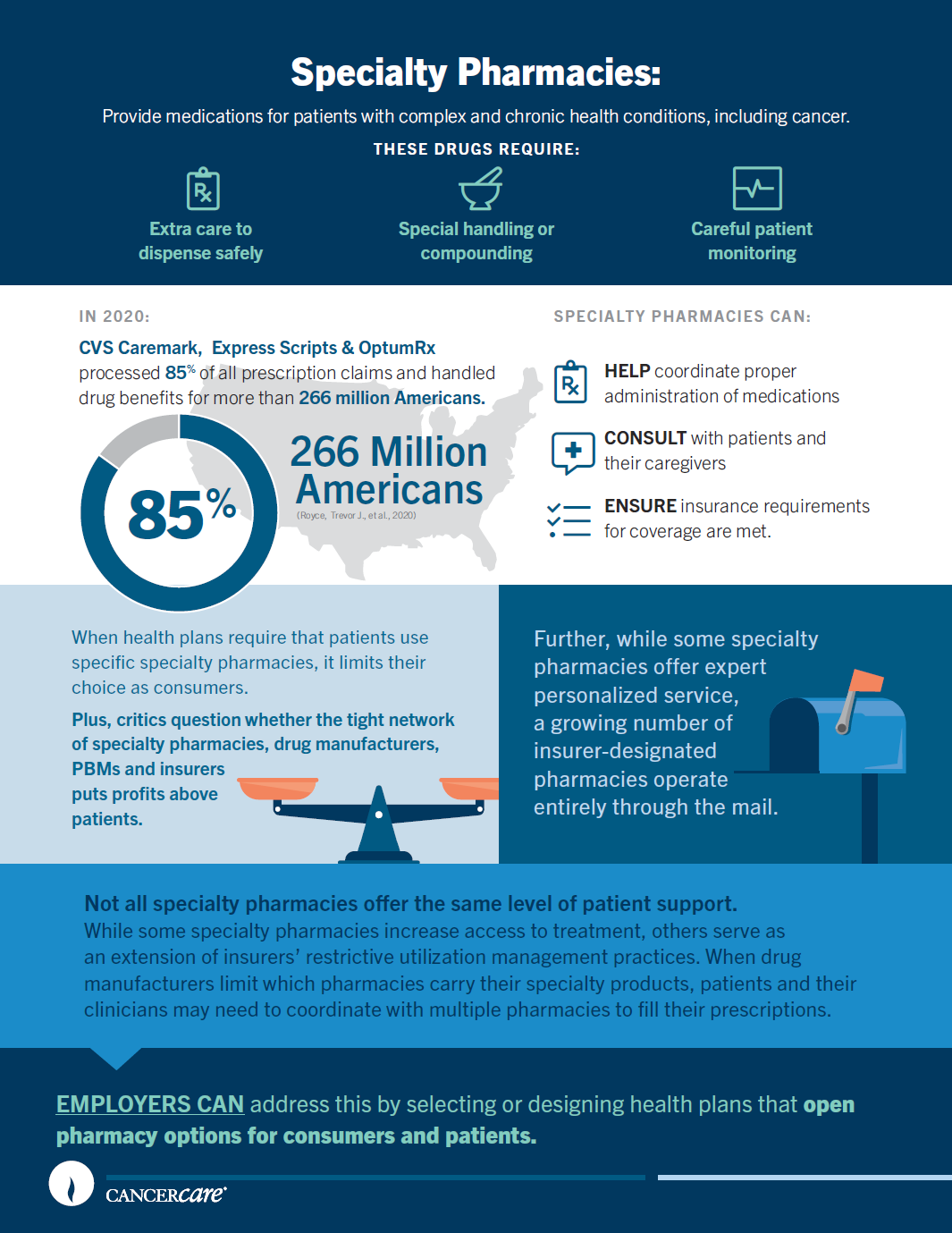

What are specialty pharmacies?

Specialty pharmacies focus on medications for complex, chronic or rare medical conditions, including cancer. These drugs require extra care to dispense safely. They may need temperature-controlled storage or special handling, delivery by injection or infusion, or on-going patient monitoring. For cancer patients, specialty pharmacies can help coordinate the shipment of chemotherapeutics and the logistics of how they’ll be administered.

While there is no official licensure to designate specialty pharmacies, some seek accreditation from independent organizations, such as the Center for Pharmacy Practice Accreditation or the Accreditation Commission for Health Care, to demonstrate their high quality of care. Not all specialty pharmacies offer the same level of patient support. While some specialty pharmacies increase access to treatment, others serve as an extension of insurers’ restrictive utilization management practices.

Why do insurers use specialty pharmacies?

Since the 1990s, the rise of new specialty drugs—and their costs—has turned once-niche specialty pharmacies into a growing industry. Their services have attracted insurance providers, pharmaceutical benefit managers and drug manufacturers who see the profit potential. Insurers and PBMs negotiate contracts with, own or control specialty pharmacies to serve as designated providers for their health plans. The pharmacy agrees to reimbursement rates that are more profitable for the insurer or PBM, in exchange for access to a larger pool of patients. On the other side of the supply chain, some drug manufacturers set up contracts that grant a few pharmacies exclusive access to carry their products, helping to control pricing and ensure safe delivery of sensitive medications.58,59

Since the 1990s, the rise of new specialty drugs—and their costs—has turned once-niche specialty pharmacies into a growing industry. Their services have attracted insurance providers, pharmaceutical benefit managers and drug manufacturers who see the profit potential. Insurers and PBMs negotiate contracts with, own or control specialty pharmacies to serve as designated providers for their health plans. The pharmacy agrees to reimbursement rates that are more profitable for the insurer or PBM, in exchange for access to a larger pool of patients. On the other side of the supply chain, some drug manufacturers set up contracts that grant a few pharmacies exclusive access to carry their products, helping to control pricing and ensure safe delivery of sensitive medications.58,59

Concerns about specialty pharmacies

When health plans require that patients use specific specialty pharmacies, it limits their choice as consumers. Further, while some specialty pharmacies offer expert personalized service, a growing number of insurer-designated pharmacies operate entirely through the mail. Patients report difficulties refilling prescriptions, suffer long waits to reach customer service representatives and experience life-threatening shipment delays and dosage errors for critical drugs. Consumer Watchdog, a consumer advocacy group, has sued several insurance providers on behalf of patients taking HIV medications, alleging that restrictive specialty pharmacy requirements were discriminatory.

When drug manufacturers limit which pharmacies carry their specialty products, patients and their clinicians may need to coordinate with multiple pharmacies to fill their prescriptions.58 Worse, they may discover that the drug best suited to a patient’s treatment is not carried by the pharmacies in their insurer’s network.60

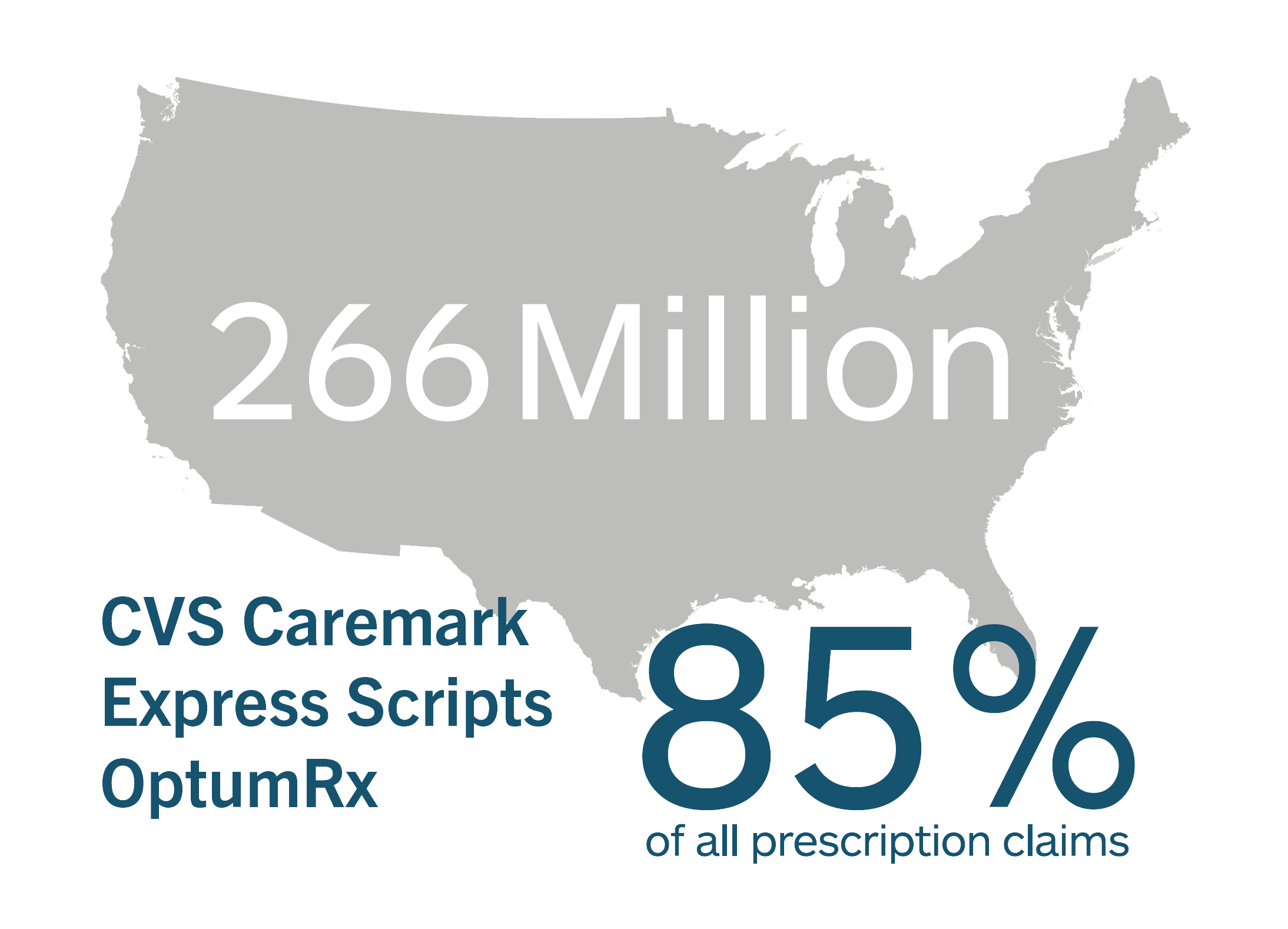

Critics question whether the tight network of specialty pharmacies, drug manufacturers, PBMs and insurers puts profits above patients. In 2020, the three largest PBMs—CVS Caremark, Express Scripts and OptumRx, all owned by health insurers—processed 85% of all prescription claims and handled drug benefits for more than 266 million Americans.7 Insurers can require patients to fill prescriptions at a pharmacy they run, while also setting patient copay rates and out-of-pocket caps. Some patient advocates worry this poses a conflict of interest that acts as a disincentive for insurers and PBMs to keep costs low for patients. 7,61

Specialty pharmacies fact sheet infographic

For patients: What Is a Specialty Pharmacy? fact sheet

Not all specialty pharmacies offer the same support. While some offer expert personal services, others just mail the medications. Learn more about specialty pharmacies and what you should do if you have concerns. View our fact sheet >>

Common UM Practices & Consequences

Copay Accumulator Programs

What are copay accumulator programs?

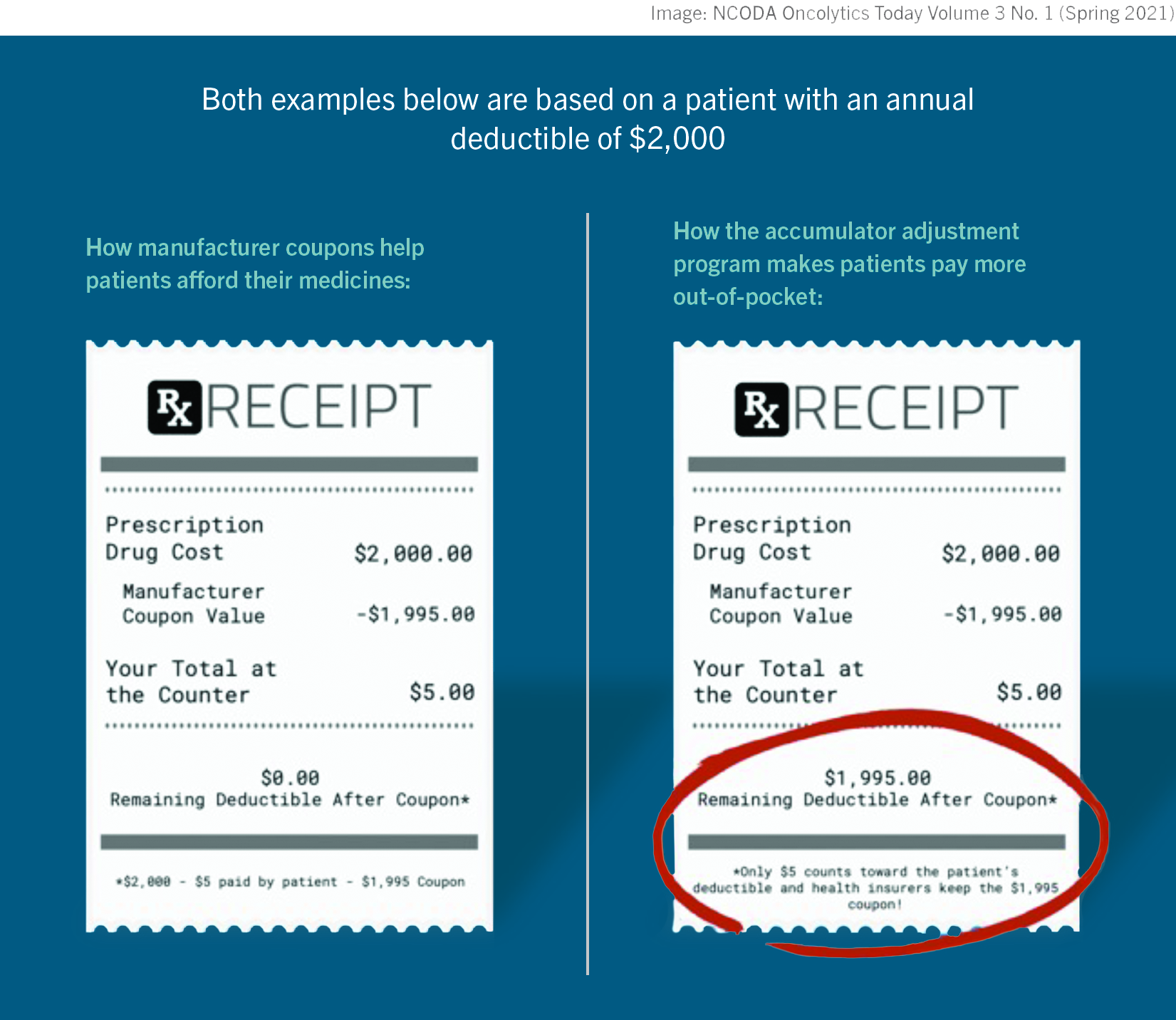

Copay accumulator programs, a recent addition to the insurance UM landscape, radically change the way patients with serious conditions pay for medications. Patients taking high-cost drugs often rely on drug manufacturer coupons or funds from charities like CancerCare to cover expenses their pharmacy benefits do not. Typically, the dollar amount of this copay support counts towards the patient’s annual out-of-pocket spending maximum and moves them closer to reaching their deductible. But under copay accumulator programs, insurers no longer count copay support toward a patient’s out-of-pocket maximum and deductible.

This means it takes patients longer and costs them more to reach the point where insurance helps pay for covered drugs. And when copay support is no longer available, the patient must pay their copay in full until their deductible is finally met. This can be hundreds to thousands of dollars, even for a single prescribed medication.

Ultimately, copay accumulator programs are “only adding more financial strain for patients who may be facing hardships due to the coronavirus pandemic’s impact on jobs and family budgets.”62

Patients who receive copay support report being caught off-guard by the new accumulator policies. Consider this: for the first few months of the year, you fill your prescription for a drug that is in a high cost-share tier, contributing $20 toward each copay and using a manufacturer copay coupon to cover the rest. Then, when you pick up your prescription in April, you’re told you owe $3,000. You’ve used up the coupon, your deductible has not yet been met and you’re now solely responsible for the prescription’s full monthly cost-share amount. When that happens, you have three choices: scramble to cover the unexpected cost; contact your physician to find a lower-cost treatment, which may not be possible; or walk away without the medication.

“Copay accumulator adjustment policies put patients with chronic conditions in a tough position—forcing them to choose between their health and other financial obligations.”62

With more than one-third of commercially insured Americans in health plans that include a copay accumulator program of some form,63 you might wonder how such a pivotal policy change could catch people by surprise. One reason is that health plans don’t identify “copay accumulator programs” as such. Rather, insurers may refer to “coupon adjustment,” “variable copayment,” an “out-of-pocket maximum calculation process” or “pharmacy coupon adjustment changes”; others call it an “Out of Pocket Protection Program,” “Benefit Plan Protection Program” or “Copay Card True Program Accumulation.”63,64 There is no standard industry term used to help consumers quickly identify copay accumulator programs in action.

In a survey by McKesson, 60% of patients believed copay accumulator programs were a benefit to them65; in reality, however, they benefit the health plan. The American Society of Clinical Oncologists agrees that the language used for copay accumulator programs is misleading: “While they are described as a benefit for patients, these programs in effect prevent patients from reaching their deductibles sooner. Copay accumulator programs generate large savings for employers and PBMs while increasing cost-sharing for patients.”66 Copay accumulator programs also provide insurers and PBMs with a financial boost, allowing them to “double dip” on deductibles. Even after the insurer collects the full deductible through a patient’s manufacturer coupons or other financial assistance, they still require the patient to pay the deductible in full (again) out of their own pocket.

Concerns about copay accumulators

Insurers and PBMs argue that manufacturer coupons for brand-name drugs undermine formulary design and increase spending by undercutting the cost savings offered by generic drugs. By requiring that patients pay more for brand-name drugs without using copay support—in a sense, putting more “skin in the game”—insurers and PBMs believe patients will seek out lower-priced drug options. This rationale, however, is flawed in several ways.

First, the brand-name drugs that patients rely on may not have cheaper alternatives. One study found that the majority of brand-name drugs with copay coupons have no lower-cost generic equivalents.67 Many oncology drugs do not have substitutes that are both equally effective and less expensive for patients.

Second, many patients delay or abandon treatment when faced with higher cost sharing, leading to expensive medical complications later. Numerous studies have found that higher out-of-pocket costs are associated with lower rates of filling prescriptions, delays in refilling prescriptions, higher rates of not taking medications as prescribed or abandoning them entirely.10 Patients who delay or abandon their drug treatment are at higher risk for expensive emergency care, avoidable hospitalizations and poorer health outcomes. Employers who choose health plans that use copay accumulators may see these costs reflected in increased illness-related absences and declines in productivity.

In contrast, improving drug coverage and reducing patients’ out-of-pocket costs, including through the use of copay support, improves medication adherence and reduces the rate of expensive emergency care and hospitalization.68,69

Adam J. Fein, CEO of Drug Channels Institute, summarizes the situation this way: “Higher utilization of specialty drugs is usually considered a positive trend. That’s because it’s well established that pharmaceutical spending reduces medical spending and improves patients’ health. Given the massive cost-shifting to patients, I expect that copay accumulators will reduce spending by decreasing the utilization of specialty drugs.”70 That is to say, short-term savings will come at the expense of patients’ long-term health and survival.

“Given the massive cost-shifting to patients, I expect that copay accumulators will reduce spending by decreasing the utilization of specialty drugs.”

- Adam J. Fein

CEO of Drug Channels Institute

Meet the copay maximizer

To buffer the financial burden of copay accumulators, insurers have now started to adopt copay maximizer plans.71 Like an accumulator, a copay maximizer does not count copayment financial assistance toward the patient’s deductible and out-of-pocket maximum. The difference is that maximizer plans apply the value of the coupon or charitable support evenly throughout the benefit year, rather than using it up and then abruptly shifting all costs to the patient, as the accumulator does. Depending on the maximizer plan and type of copay support, some patients’ out-of-pocket costs may be eliminated or so low that they never reach their annual deductible or maximum. A patient might still pay more overall than they did with copay support, but much less than they would under a copay accumulator.

While copay maximizer plans are more “patient friendly,” some come with restrictive requirements. Under maximizer plans, insurers and PBMs set the copay amount for drugs at the maximum value of the copay support, rather than basing it on the drug’s list price.71 So, a drug with a coupon that has a maximum annual value of $20,000 would cost a patient $20,000 annually to fill—regardless of their plan’s out-of-pocket maximums. To avoid that huge cost, patients have to enroll in the copay maximizer plan, which is handled by a separate business under contract with the insurer or PBM. These third-party businesses label high-cost specialty drugs as “non-essential health benefits,” a designation that removes the out-of-pocket limits required by the Affordable Care Act to protect patients.71 Confusing? Pharmaceutical industry watchdogs agree.

Are copay accumulators legal?

Although CancerCare, the American Medical Association, the American Society of Clinical Oncology and other leading medical organizations oppose copay accumulator programs, these plans received legal support from the U.S. Department of Health and Human Services and the Centers for Medicare and Medicaid Services (CMS) in 2021 policy determinations.

Despite the CMS ruling, industry experts warn that copay accumulator programs may violate other federal laws that protect employees, patients and consumers, due to misrepresentation, lack of transparency, discriminatory practices, violations of patient privacy, and out-of-pocket maximums. Employers that choose health plans with copay accumulator programs may be putting themselves at greater risk for liability.

The CMS ruling also leaves space for states to pass their own regulations on copay accumulator programs and, as policymakers recognize the harm of these practices, a growing number of states have moved to ban their use. As of July 2021, 11 states and Puerto Rico have enacted laws to restrict copay accumulator programs. Kentucky, for example, limits use by permitting accumulators only for drugs with generic alternatives, while granting doctors greater control to deem a brand-name drug medically necessary. However, state regulations do not extend to self-insured employer plans, so healthcare experts, physician groups and patient advocates strongly urge employers to reject or remove copay accumulators in their health plan design.

Case study: Copay accumulators, Jen & Penny Hepworth

Jen & Penny Hepworth

Jen & Penny Hepworth

Salt Lake City, Utah

Ankylosing spondylitis & cystic fibrosis

Watch Jen tell her story »As a mother to two beautiful daughters and two wonderful stepsons, I want to provide a home filled with happy memories and vacations, but our medical costs have prevented us from doing so. Living with ankylosing spondylitis is not easy, and the combination of my disease and my daughter’s cystic fibrosis wreaks financial havoc on our lives.

Ankylosing spondylitis is an autoimmune disease that affects my spine and all of my major joints. To stay healthy and avoid pain, I’ve been prescribed monthly immunosuppressants for years. On average, these cost about $10,000 per month. I also take daily pills prescribed by my doctor.

In addition to my health challenges, my daughter was diagnosed with cystic fibrosis at three weeks old; she has two genetic mutations called DF508 and G551D. She was given a life expectancy of 41 years. As a parent, this is obviously something you never want to hear.

Of course, we wanted to throw everything we had at this disease to give our baby girl the best life possible. The doctors put her on a medication called Kalydeco at two years old. This medication costs $300,000 annually. She’s now eight and recently switched to a CFTR modulator called Trikafta, which nets out at $311,000 a year.

As an average American family living north of Salt Lake City, Utah, we do not have the finances to cover the overwhelming cost of these medications. Despite the fact that my husband is a very successful engineer, we’ve never had the chance to enjoy his financial gains due to the policies enforced by his employer’s insurance company. All I want is for our children to have positive family memories, but the monetary burden we carry from the insurance company continues to get in the way.

The state of Utah allows insurance companies like ours to use a copay accumulator. Without any background, it sounds like a positive policy for the insured. We quickly found out that was not the case. This policy is used by PBMs/insurance companies to decrease costs for the insurer and increase costs for the insured. When manufacturers offer discounts or coupons on medications, the insurance company prevents those discounts from applying to patients’ deductibles and their maximum out-of-pocket spend. Since people end up paying much more than if the insurance company counted that support, the policy results in patients delaying or not seeking treatment.

Our family has struggled under this policy. Without modulator drugs, a CF patient can expect annual hospital stays up to 14 days long and routine respiratory clean outs as the baseline—when symptoms present themselves, it only results in more doctors and more treatments. This all adds up. For our family, the only way we’ve been able to keep our daughter’s hospital visits to a minimum is to keep her on these expensive drugs. The only way we’ve been able to maintain access to these drugs is through financial aid from a multitude of sources. Between the two of us, we see rheumatologists, EMTs, a pulmonologist, a gastroenterologist, a social worker, a dietician and a respiratory therapist on a regular basis. Not to mention the daily pills and monthly injections that help us function. The financial burden of these treatments and the lack of support from our insurance company has us living paycheck-to-paycheck.

We’re not the only ones to suffer under copay accumulators—many patients struggle to feed their families and have more severe situations than us. It’s a challenging situation that could easily be changed if the insurance companies supported their beneficiaries instead of lining their own pockets.

Copay accumulator fact sheet infographic

For patients: What Are Copay Accumulator Adjustor Programs? fact sheet

Every health insurance plan requires “cost-sharing” by a patient. Learn more about terms, how copay accumulator programs work and what to look for in your health insurance documents. View our fact sheet >>

Common UM Practices & Consequences

The Appeals Process

When insurers deny coverage

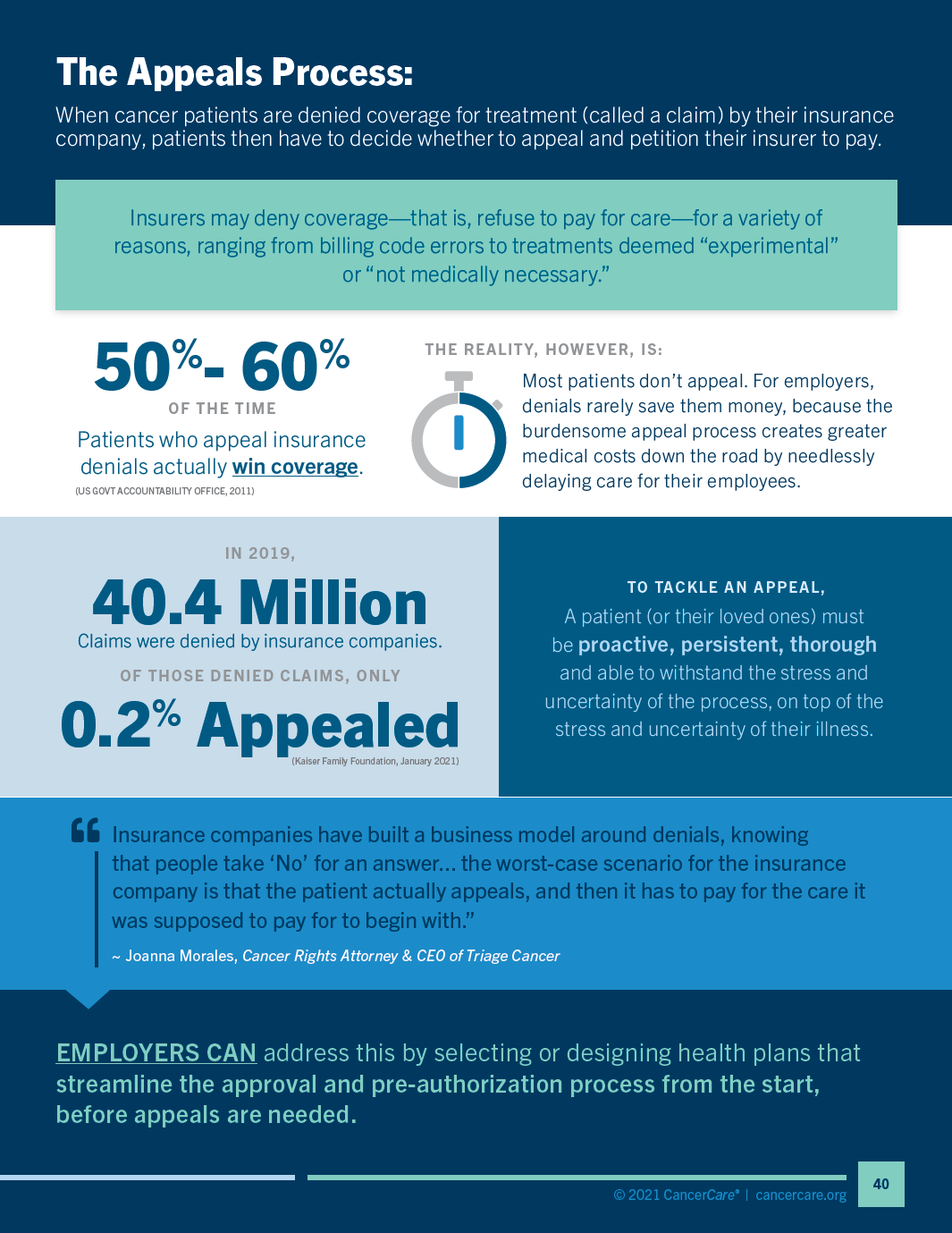

At some point, nearly all cancer patients will find their insurance plan has denied coverage for a prescribed medical service (called a claim). It could be a test, treatment, scan, surgery, procedure, medication or other care. Patients then have to decide whether to appeal and petition their insurer to pay.

Patients who appeal insurance denials actually win coverage an estimated 50-60% of the time.72 Yet a review of 40.4 million claims denied by insurance companies in 2019 found that patients appealed only 0.2%.73

Why are claims denied?

The majority of denials stem from administrative issues: mistakes in coding, missing forms, incomplete billing or patient info, duplicate or overlapping claims, and late submissions. Other denials are due to claims that don’t follow the insurance plan’s rules and limits: for instance, lack of proper pre-authorization or exclusion from coverage altogether.

A small number of claims, though significant for cancer patients, are denied based on their perceived medical value as “unproven,” “experimental,” “investigational” or deemed “not medically necessary” for a patient’s condition. Yet, insurer assessment may not (intentionally, perhaps) be keeping pace with cancer care innovation and increasingly customized treatments. Proton therapy, for instance, is a newer alternative to traditional radiation therapy that limits damage to healthy tissue while targeting cancer cells. For some patients with brain tumors, it could be an optimal treatment. But many major insurers refuse to cover proton therapy. 74

The U.S. Inspector General recently probed the efficacy and accuracy of denials in an audit of Medicare Part D insurers. In 2017, 35% of pre-authorization requests for medications were initially denied.

Among the denied requests that patients appealed, insurers later approved a whopping 73%—“suggesting that many initial denials of coverage are inappropriate.”28

Surprisingly, receiving pre-authorization for care is not a guarantee that an insurer will pay for it. A pre-approved claim may be rejected later: a “retrospective denial.” With pre-authorization requirements on the rise, so are cases of retrospective denials that leave patients with hefty surprise bills. These denials can happen when the insurer objects to how billing was handled, indicates the procedure was performed too long after approval was granted, or determines after further review that the care was not medically necessary.75

Designing benefits with stronger coverage and fewer UM controls—that is, health plans that avoid restricted formularies, heavy pre-authorization requirements and step therapy protocols—helps to reduce the number of denials employees encounter.

What it takes to appeal: the added cost of time & stress

To tackle an appeal, a patient (or their loved ones) must be proactive, persistent, thorough and able to withstand the stress and uncertainty of the process, on top of the stress and uncertainty of their illness. Patients often need to relay information between their doctor and the insurer to coordinate numerous details; for example, making sure any related bills aren’t sent to a collection agency, which would hurt the patient’s credit rating.

In the best case scenario, patients may be able to resolve administrative issues with an insurance representative over the phone—most likely after several lengthy calls—and resubmit the claim without going through a formal appeal. Other denials, particularly those regarding medical necessity, require a formal and often arduous written appeal and supporting evidence to make a strong case for coverage. It typically requires the healthcare team to gather documentation, which may include data from medical records and clinical studies, to back up the rationale for prescribed care. If a claim is still rejected after appealing, some plans allow for a second internal appeal, or a patient can file an external appeal with state-certified reviewers, independent from the insurer, who deliver a final decision.

Patients waiting on appeal decisions find themselves in healthcare limbo. Do they continue with treatment, not knowing how much they may have to pay? Or do they delay care, not knowing how their condition may worsen? It can take 30 days for pre-authorization appeals to be adjudicated and 60 days for post-treatment appeals. In emergency or critically time-sensitive cases, patients can start an external appeal at the same time as their internal appeal to expedite a final decision in a matter of days. Clear timelines for decisions are crucial. Some employers now have clauses that automatically require insurers to cover a prescription if an appeal decision is not delivered by a set time.